Mortgage on Real Estate: what it is, how it originates, how it is deleted, and what it means for the buyer

TL;DR:A mortgage is a legally registered lien on real estate by which the creditor secures the collection of claims, and it arises from registration in the land registry. Deleting a mortgage requires the issuance of a deletion statement after debt repayment and a court procedure that lasts from 3 to 10 weeks, with costs ranging from 30 to 250 euros. Buyers must check Part C before purchasing and ensure the burden is deleted so that the property is free of encumbrances and legally secure.

A mortgage is a legally registered lien on real estate by which the creditor, most often a bank, secures the collection of its claim in the event that the debtor fails to fulfill credit obligations. In the Croatian real estate mortgage system, this right arises from registration in the land registry and directly affects ownership rights, the possibility of sale, and the legal status of every property. Without understanding this mechanism, buyers and sellers risk costly legal complications that can stop or annul the entire transaction.

What is a real estate mortgage and how does it originate?

A mortgage is a form of real right over another's property by which a monetary claim is secured. In practice, when you take out a housing loan, the bank does not become the owner of the property, but acquires the right to forced collection by selling that property if you stop repaying the loan.

A mortgage is the most common instrument for securing housing loans in Croatia and is regularly combined with an assigned insurance policy and a promissory note. This means that you sign multiple security instruments at once, and a mortgage is just one of them.

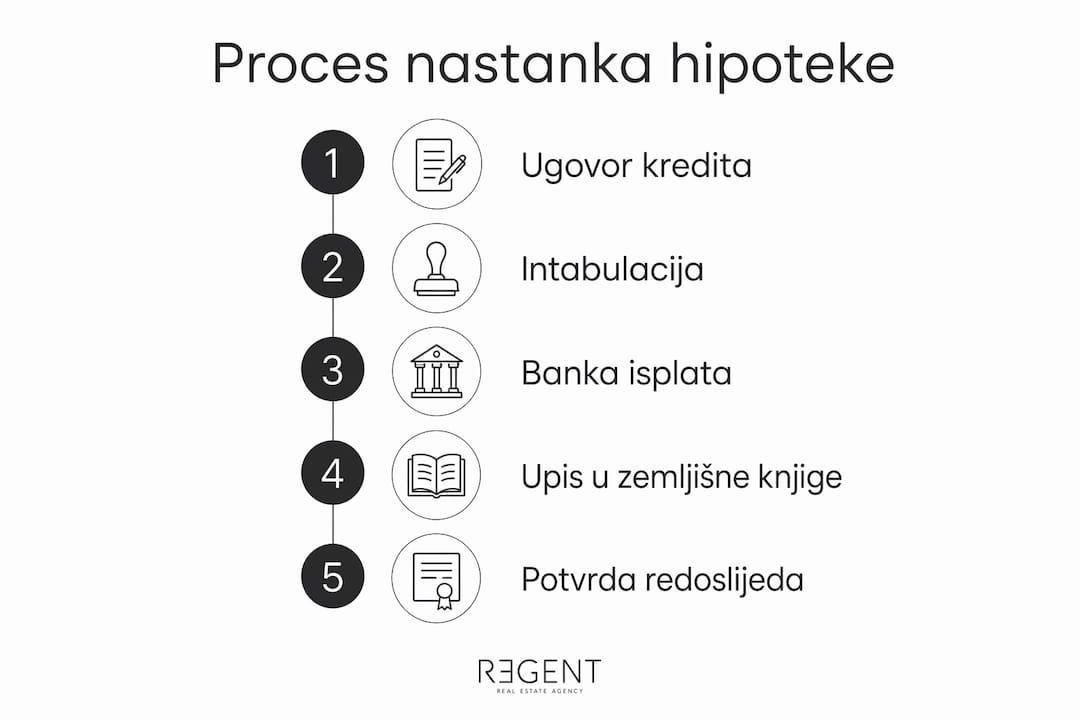

The legal term for registering a mortgage in the land registry is intabulation. The procedure is carried out before the competent municipal court or through a public notary, and the result is a visible entry in Part C of the land registry entry, which is called an encumbrance sheet. Every buyer must check this specific sheet before signing any contract.

Timeline of mortgage origination

The order of steps for mortgage origination typically looks like this:

- The buyer and seller sign a pre-contract or sales contract

- The buyer submits a housing loan application to the bank

- The bank appraises the property and approves the loan conditional on mortgage registration

- The loan agreement and mortgage agreement are solemnized by a public notary

- A request for mortgage registration is submitted to the land registry department of the competent court

- The bank disburses the loan only after the mortgage has been registered in the land registry

This order has a practical consequence: the seller does not receive the money immediately, but only when the bank confirms the proper registration. Coordination between the buyer, seller, and bank at this stage is essential to avoid transaction delays.

Professional advice: Before signing the loan agreement, request a written confirmation from the bank regarding the exact disbursement order and the conditions that must be met. This will help you realistically plan the property takeover date.

How is a mortgage deleted and how much does it cost?

A mortgage remains on the property until a formal deletion procedure is carried out, even if the loan has been fully repaid. Deletion is not automatic and requires an active approach from the property owner. Missing this step means that the property still carries an encumbrance in the land registry, which can block its sale or burden a new buyer.

The legal document that initiates the deletion of a mortgage is called a deletion statement. The bank is obliged to issue a deletion statement within 30 days of the final loan repayment. The deletion statement must contain accurate information about the mortgage, including the land registry entry number, the amount of the claim, and the identification of the parties. The court verifies its validity, and any irregularity can significantly delay the process.

Steps for mortgage deletion

- Repay the loan in full and request a written confirmation from the bank about the debt settlement

- The bank issues a deletion statement within the legal period of 30 days

- The deletion statement is solemnized by a public notary (not always mandatory, but recommended)

- You submit a proposal for mortgage deletion to the competent municipal court

- The court verifies the correctness of the documentation and issues a decision on deletion

- The mortgage is deleted from Part C, and the property becomes free of encumbrances

Mortgage or fiduciary transfer of ownership: what's the difference?

There are two fundamental differences that every property buyer must understand.

With a mortgage, the ownership of the property remains with the debtor — the bank only acquires a lien right, visible in Part C (encumbrance sheet). In the case of a fiduciary transfer of ownership, the debtor temporarily transfers ownership to the bank, which is recorded in Part B (ownership title). This is not a semantic difference — it is a difference in the degree of legal protection.

A mortgage is legally more clearly regulated, provides higher protection to the debtor, and is the dominant instrument for securing housing loans in Croatia. Fiduciary transfer is becoming rarer precisely because the bank formally becomes the owner of the property, which in case of a dispute can create complex legal situations to the detriment of the debtor.

For property buyers, this means one thing: always check both Part B and Part C. A mortgage is visible in the encumbrance sheet, while a fiduciary transfer changes the ownership title.

Missing this check is not just a mistake — it can be costly.

What does a mortgage mean for a buyer purchasing a property with an encumbrance?

Purchasing a property with a registered mortgage is possible, but it requires special attention and legal preparation. Ownership of a property is acquired exclusively through registration in the land registry, and encumbrances like mortgages are shown in Part C, which every buyer must review before signing a contract. An unverified encumbrance that remains on the property after purchase becomes the problem of the new owner, not the seller.

There are three common ways to resolve a mortgage during a sale:

- Mortgage repayment from the purchase price: A part of the purchase price is paid directly to the bank to settle the remaining debt, and the rest goes to the seller. For example, if the purchase price is 200,000 € and the remaining debt is 60,000 €, the buyer pays 60,000 € to the bank, and 140,000 € to the seller.

- Assumption of mortgage: The buyer assumes the seller's credit obligations with the bank's consent. This is less common and requires a specific credit analysis of the buyer.

- Mortgage deletion before sale: The seller repays the loan from their own funds or a new loan, obtains a deletion statement, and deletes the mortgage before signing the sales contract.

The legal implications are serious if a mortgage remains registered after purchase. The bank retains the right to forced collection and can initiate enforcement proceedings against the property regardless of who the new owner is. This scenario is not theoretical; it happens when buyers do not check the status of the land registry or when the mortgage deletion is not carried out within the agreed deadline.

Professional advice: Always request a document verification of the property by a lawyer or real estate agency before signing a pre-contract. Specifically check Part C and ask the seller for a written statement regarding the debt status with the bank.

Croatian regulatory bodies, specifically the Croatian National Bank, have introduced macroprudential measures that limit the LTV ratio to 80% and the DTI ratio to 50% of total income. This means that the bank cannot approve a loan that exceeds 80% of the property's value, which directly affects the mortgage amount and buyer protection in case of falling market prices. For buyers planning to purchase a property with a mortgage, it is advisable to use a mortgage calculator Croatia offered by banks to pre-estimate the total loan costs and the potential amount of the mortgage burden.

Key Insights

A mortgage is a legal encumbrance that remains on a property until formally deleted from the land registry — regardless of loan repayment or change of ownership.

Mortgage Origination — A mortgage originates by intabulation in Part C, and the bank disburses the loan only after the registration is formally completed.

Mortgage Deletion — Deletion requires a deletion statement from the bank and a court procedure that takes 3 to 10 weeks. The procedure is not automatic and the owner must actively initiate it.

Deletion Costs — Total costs range between 30 € and 250 €, including court and notary fees.

Purchasing with Encumbrance — The buyer must check Part C and arrange for mortgage deletion before or during the sale. An encumbrance that remains on the property becomes the problem of the new owner.

Mortgage vs. Fiduciary Transfer — A mortgage is a safer and more transparent security instrument than a fiduciary transfer of ownership, offering higher legal protection for the debtor.

Regent's Expert View on Mortgages in Real Estate Transactions

From experience working with buyers and sellers across Croatia, I can say that misunderstanding mortgage encumbrances is one of the most common causes of complications in real estate transactions. Buyers often assume that a property is free of encumbrances simply because the seller claims the loan has been repaid. Without access to an up-to-date land registry extract, this assumption can be a costly mistake. I particularly caution against situations with multiple registered mortgages on one property. Planning the deletion order and coordinating with multiple banks requires precise administrative preparation and knowledge of the real estate purchase process from start to finish. Deadlines are strict, and any error in the documentation can delay the entire process by weeks. Newer regulations and HNB's macroprudential measures have brought greater protection for buyers, but also stricter lending conditions. This is a positive change, but it requires buyers to be better informed than ever. The role of a public notary in solemnizing contracts and verifying documentation is not a formality, but a real protection for all parties in the transaction. My opinion is that every real estate transaction with a mortgage requires expert accompaniment from day one, not just when problems arise.

— Regent

How Regent can help you with buying or selling a property with a mortgage

Regent provides comprehensive support to buyers and sellers of real estate in all phases of a transaction, including cases with mortgage encumbrances. Our team checks the status of land registers, coordinates communication with banks and public notaries, and ensures that every step is legally sound. Browse our property portfolio and find a property that suits your needs. For more complex cases involving mortgages, our legal services cover encumbrance verification, document preparation, and representation in court proceedings.

FAQ

What is a real estate mortgage?

A mortgage is a legally registered lien on real estate by which a bank secures the collection of a housing loan. It is registered in Part C of the land registry entry and remains visible to all third parties.

How is a mortgage deleted after loan repayment?

After loan repayment, the bank issues a deletion statement within 30 days. The property owner submits the deletion statement to the competent court, which then issues a decision on the deletion of the mortgage from the land registry.

How much does it cost to delete a mortgage in Croatia?

The total costs of deleting a mortgage range between 30 € and 250 €, and the procedure takes 3 to 10 weeks depending on the court and the complexity of the case.

Can I buy a property that has a registered mortgage?

Yes, purchasing is possible. The usual solution is for a portion of the purchase price to be paid directly to the bank to settle the debt, and the mortgage is deleted as part of the transaction or immediately before it.

What is the difference between a mortgage and a fiduciary transfer of ownership?

With a mortgage, ownership remains with the debtor, and the bank only has a lien right visible in Part C. With a fiduciary transfer of ownership, ownership temporarily transfers to the bank, which carries greater legal risk for the debtor and less transparency towards third parties.

Recommended

- Property Registration in Croatia: what it is, how it works, and what you need to know?

- When to Buy Property: A Market Analysis Guide

- Guide to buying real estate in Croatia for foreign citizens