Summary

Briefly: Buying property for retirement requires a focus on location, accessibility, and security. Additional costs can amount to up to 12% of the price, including tax, commissions, and legal due diligence costs. Ensure legal security and documentation compliance to avoid financial losses and legal issues. Buying property for retirement is defined as a strategic decision by which retirees or pre-retirees secure a stable home adapted to the needs of old age. Unlike buying at a younger age, here the priorities are different: accessibility of space, proximity to healthcare, legal security, and long-term financial sustainability within a fixed retirement budget. Croatia offers diverse options, from apartments in cities with developed infrastructure to peaceful coastal and rural areas. Each of these options carries specific advantages and challenges that are worth thoroughly considering before making a decision.

Key facts

- Buying a property for retirement requires aligning location, accessibility of space, financial sustainability, and legal security to be a long-term stable decision.

- Location and Accessibility

- Proximity to healthcare and a ground floor or elevator are crucial for quality of life in old age.

- Total Purchase Costs

- Additional costs amount to 7%–12% of the price, which for a property of €200,000 means up to an additional €24,000.

- Financing with a Loan

- Banks shorten the repayment period for older buyers, which increases monthly installments and requires greater creditworthiness.

- Legal Review

- Checking the ownership deed, occupancy permit, and cadastral data prevents the loss of earnest money and legal problems.

- City or Quiet Environment

- Cities offer better healthcare infrastructure, while quiet environments offer lower prices and a good quality of life, provided that the winter availability of services is checked.

Buying Real Estate for Retirement and the Third Age

In brief: Buying real estate for retirement requires a focus on location, accessibility, and security. Additional costs can amount to up to 12% of the price, including tax, commissions, and legal due diligence costs. Ensure legal security and documentation compliance to avoid financial losses and legal problems.

Buying real estate for retirement is defined as a strategic decision by which retirees or pre-retirees secure a stable home adapted to the needs of the third age. Unlike purchasing at a younger age, priorities here are different: space accessibility, proximity to healthcare, legal security, and long-term financial sustainability within a fixed retirement budget. Croatia offers diverse options, from apartments in cities with developed infrastructure to peaceful coastal and rural areas. Each of these options carries specific advantages and challenges that are worth thoroughly considering before making a decision.

What are the key criteria for buying real estate in retirement?

Location is the most important criterion when choosing real estate for the third age. Proximity to general practitioners, pharmacies, hospitals, and daily amenities such as shops and markets directly affects the quality of life. Retirees who move to a quiet rural area often realize only after several years that healthcare services are unavailable without a car.

Accessibility of space without architectural barriers is equally important. A ground-floor apartment or an apartment with an elevator significantly eases daily life for people with limited mobility. Wide hallways, low thresholds, walk-in showers, and grab bars in the bathroom are not luxuries, but practical necessities that become increasingly important with age.

Home and neighborhood security is the third key criterion. Quiet residential areas with good lighting, familiar neighbors, and accessible emergency services provide a sense of security that is particularly valuable for older people. The size of the property is often underestimated. Buying an oversized property for the third age brings multiple hidden costs of heating, cooling, and maintenance. It is recommended to choose a home aligned with actual daily needs, not with occasional family visits.

- Location: proximity to healthcare, pharmacies, markets, and public transport

- Accessibility: ground floor or elevator, no high thresholds, adapted bathroom

- Security: quiet neighborhood, good lighting, familiar community

- Size: aligned with actual needs, not ideals

- Infrastructure: check availability of services outside tourist season

Professional advice: Before buying, visit the property at different times of the day and week. Check how far the nearest pharmacy and doctor's office are, and whether public transport is available if you stop driving.

Financial aspects of buying real estate for retirees

Buying real estate in retirement entails costs that far exceed the purchase price itself. Total additional costs of buying real estate in Croatia amount to 7%–12% of the purchase price. For a property worth €200,000, this means between €14,000 and €24,000 in additional costs that need to be planned in advance. Here's what's included in that amount:

- Real estate transfer tax: a rate of 3% is paid on all properties except new constructions from companies in the VAT system, where VAT is already included in the price.

- Down payment: amounts to about 10% of the purchase price and is paid immediately in cash. Buyer withdrawal means forfeiture of the down payment.

- Agency commission: usually 2%–3% of the purchase price.

- Notary fees: can be negotiated and vary up to €500, so it is advisable to request offers from multiple notaries.

- Attorney fees and expert inspections: expert inspection and geodesic measurement can cost from several hundred to over a thousand euros.

Buying versus renting: what is better for retirees?

Buying provides security and protection against rising rents, but requires large initial capital and reduces liquidity. Renting maintains financial flexibility and does not tie up capital, but neither builds equity nor provides long-term housing security. For retirees with sufficient capital and a clear desire for a stable home, buying is a more favorable long-term option. For those unsure where they want to live or planning seasonal changes of residence, renting may be a more reasonable choice. Financing through loans for older buyers carries specific challenges. Banks limit the repayment period for individuals aged 45 and over, resulting in shorter terms and higher monthly installments. Retirees planning loan financing must account for a greater burden on their fixed budget. Real estate as protection against inflation is only valid if ongoing costs are sustainable. Reserves, utilities, and occasional repairs can be a significant burden on a fixed pension, so a detailed analysis of monthly costs is crucial before signing a contract.

Legal aspects of buying real estate for the third age

The legal security of a purchase depends on a thorough review of documentation. Engaging a lawyer is crucial for verifying ownership status, occupancy permit, and the consistency of land registry and cadastral data. Inconsistencies in this data can prevent the transfer of ownership or use of the property. It is especially important to check the following:

- Title deed (ZK extract): confirms who the real owner is and if there are any encumbrances or mortgages

- Occupancy permit: without it, the property cannot be legally used or registered as a residence

- Consistency of cadastre and land registry: inconsistency of data between the cadastre and land registry documents can result in the loss of the paid down payment

- Unpaid utility bills: can transfer to the buyer if not checked before purchase

- Access road status: especially important for houses and vacation homes

A detailed list of documents to check when buying real estate helps avoid costly mistakes.

Lifetime and Until-Death Maintenance Agreements

A lifetime maintenance agreement is a specific legal instrument that elderly people use as an alternative to a classic purchase and sale. It provides accommodation and care to the recipient until the end of their life, and transfers ownership of the property to the provider after the recipient's death. An until-death maintenance agreement transfers ownership immediately, but with the obligation of care until the end of life. Both agreements must be concluded before a public notary and registered in the land registry to be legally valid.

Inheriting real estate

Inheriting real estate can be complex if not legally arranged in advance. A will or a gift agreement with a lifelong usufruct burden gives the owner control over who inherits the property. Without these instruments, inheritance proceeds according to legal rules that may not match the owner's wishes.

Professional advice: Always entrust the legal review of a property to a lawyer specializing in real estate, not just a public notary. A lawyer can identify hidden legal issues that a notary is not obligated to check.

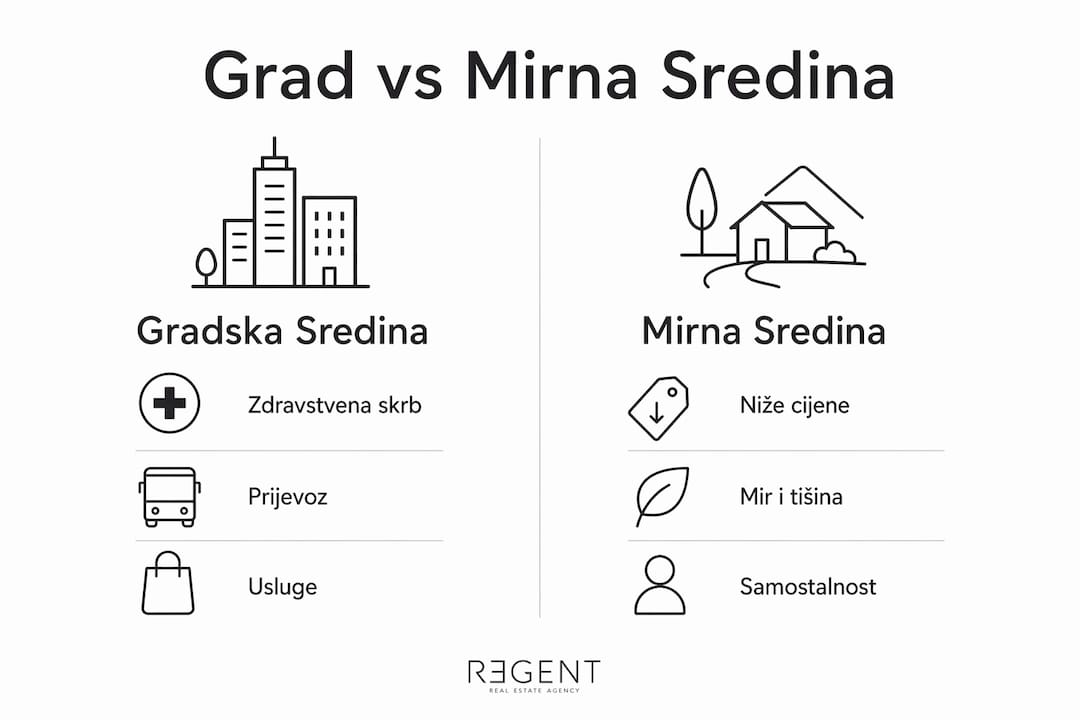

City or quiet area: what is better for retirees in Croatia?

Choosing between an urban and a quieter environment is one of the most important decisions when buying real estate for the third age. Both options have clear advantages and disadvantages.

Urban environment vs. quiet environment (coast, rural) — comparison by key criteria

Healthcare

- Urban environment: hospitals and specialists nearby

- Quiet environment: limited, often only general practice

Property prices

- Urban environment: higher, especially Zagreb and Split

- Quiet environment: lower, but rising on the coast

Public transport

- Urban environment: developed

- Quiet environment: limited or unavailable

Cost of living

- Urban environment: higher

- Quiet environment: lower, but varies seasonally

Social life

- Urban environment: diverse, cultural amenities

- Quiet environment: calmer, stronger local community

Infrastructure in winter

- Urban environment: stable

- Quiet environment: can be limited out of season

Cities like Zagreb, Split, and Rijeka offer developed healthcare infrastructure and public transport, which is crucial for older people without a car. Many choose coastal areas for the climate and quality of life, but checking local infrastructure outside the tourist season is essential before purchasing. Many places on the Adriatic have significantly fewer services available in winter than in summer.

Rural locations in inland Croatia offer lower prices and peace, but require personal transport and greater independence. For retirees planning to stay in such a property long-term, this is a factor that becomes increasingly important with age.

Key insights

Buying real estate for retirement requires aligning location, space accessibility, financial sustainability, and legal security to be a long-term stable decision.

Location and accessibility

Proximity to healthcare and a ground floor or elevator are crucial for quality of life in the third age.

Total purchase costs

Additional costs amount to 7%–12% of the price, which for a €200,000 property means up to €24,000 more.

Loan financing

Banks shorten the repayment period for older buyers, which increases monthly installments and requires greater creditworthiness.

Legal due diligence

Checking the title deed, occupancy permit, and cadastral data prevents the loss of down payments and legal problems.

City or quiet area

Cities offer better healthcare infrastructure, while quiet areas offer lower prices and quality of life, provided that winter service availability is checked.

What Regent learned working with retirees when buying real estate

Retirees seeking advice usually have a clear idea of where they want to live, but are rarely aware of how much financial and legal preparation affects the final outcome. The most common mistake is not a poor choice of property, but insufficient document verification and underestimation of ongoing costs. We have seen cases where a buyer paid a down payment for a property without a valid occupancy permit and lost money because the transfer of ownership was not possible. Such situations can be avoided if legal due diligence is performed before, not after, paying the down payment. Another common problem is buying too much space. Retirees often choose larger apartments or houses for children and grandchildren who will visit. In practice, the costs of heating, building reserves, and maintaining such properties quickly become a burden that a fixed pension cannot easily bear.

The recommendation is simple: buy a property that suits your daily needs today, not imagined needs for five years from now. Adapting the space for the third age, such as installing grab bars or replacing a bathtub with a shower, is cheaper than buying an oversized apartment that will be difficult to maintain.

— Regent

Regent as a partner in buying real estate for retirement

Regent provides comprehensive support to retirees and pre-retirees when buying real estate in Croatia. A team of experts covers legal due diligence, financial consulting, and the selection of properties adapted to the needs of the third age. For those looking for specific offers, new build apartments are available in attractive coastal locations, and the full offer is available on the property purchase page. Regent also offers legal services and financial consulting to ensure every step of the purchase is safe and transparent.

Frequently asked questions

What should be checked when buying real estate for retirement?

Check the title deed, occupancy permit, consistency of cadastral and land registry data, and unpaid utility bills. Engaging a lawyer before paying a down payment prevents costly mistakes.

How much are the additional costs of buying real estate in Croatia?

Additional costs amount to 7%–12% of the purchase price, which includes real estate transfer tax of 3%, agency commission, notary and attorney fees.

Is it better to buy or rent a property in retirement?

Buying provides long-term security and protection against rising rents, while renting maintains financial flexibility. For retirees with sufficient capital and a clear desire for a stable home, buying is a more favorable long-term option.

What is a lifetime maintenance agreement and how does it work?

A lifetime maintenance agreement obliges the care provider to care for an elderly person until the end of their life, and in return inherits their property. It must be concluded before a public notary and registered in the land registry.

How do banks treat loan applications from retirees?

Banks limit the loan repayment period for older individuals and require proof of regular income, resulting in shorter repayment periods and higher monthly installments. Retirees should expect a greater financial burden when financing with a loan.

Recommended

- When to Buy Real Estate: A Guide to Market Analysis

- Documents You Must Check When Buying Real Estate

- How to Simultaneously Sell and Buy a New Apartment

- Buying a Home with a Loan: A Guide to Costs, Interest, and Taxes